Shriram Finance has raised ₹2,000 crore through two secured Non-Convertible Debenture (NCD) issues. The company completed this fund raise after approval from its board during the meeting held on April 24, 2026. The money will support the company’s lending business and will follow all Reserve Bank of India (RBI) requirements and other statutory guidelines.

This development reflects another step in the company’s long-term funding plan. Instead of depending only on bank loans or other borrowing options, the company has chosen the debt market to secure fresh capital. This approach gives the business another source of funds while also giving investors an opportunity to earn fixed interest.

The issue includes two different NCD series. Both carry fixed annual interest rates but differ in maturity period, face value, and yield. Since both issues are secured, investors receive an added layer of protection through the assets that back these debentures.

Understanding What an NCD Means

A Non-Convertible Debenture, commonly called an NCD, is a debt instrument through which a company borrows money from investors. In return, investors receive fixed interest for a fixed period. At maturity, the company returns the principal amount.

Unlike convertible debentures, these securities do not change into company shares. Investors therefore earn fixed income instead of becoming equity shareholders. Many companies use NCDs because they provide long-term funding while investors receive predictable cash flow through regular interest payments.

For companies such as Shriram Finance, NCDs have become an important funding source because they help diversify borrowing. A diversified funding base reduces dependence on one source of capital and improves financial flexibility.

Total Fund Raise

The total amount raised stands at ₹2,000 crore.

The fund raise consists of two separate NCD options worth ₹1,000 crore each. Although both belong to the same overall transaction, each series has different financial terms.

Key Financial Details

The first option carries the series name SFL PPD 2026-27 SEP 2029.

The allotment size is 1,00,000 NCDs.

The issue size is ₹1,000 crores.

The coupon rate is 7.80% per annum.

The maturity date is September 07, 2029.

The face value of each NCD is ₹1,00,000.

The yield is 7.80%.

The second option carries the series name STFCL PP 2021-22 K-05 Further Issue 1.

The allotment size is 10,000 NCDs.

The issue size is ₹1,000 crores.

The coupon rate is 8% per annum.

The maturity date is December 26, 2031.

The face value of each NCD is ₹10,00,000.

The yield is 7.90%.

These numbers show that both issues offer fixed annual returns but differ in maturity, face value, and yield. The second option offers a slightly higher coupon but its effective yield stands at 7.90% because it carries a premium issue price.

Interest Payment Schedule

The first option follows annual interest payments.

Investors receive interest on September 07, 2026, September 07, 2027, September 07, 2028, and the final payment on September 07, 2029, which also includes repayment of the principal.

The second option also follows annual interest payments.

Investors receive interest on December 28 every year from 2026 until 2030. The final payment comes on December 26, 2031, which is the maturity date.

The effective yield for the second option remains at 7.90% because the debentures carry a premium issue price of ₹3,370 per debenture.

The scheduled payment structure gives investors clear visibility regarding future cash flow. Such certainty often attracts institutions and investors who prefer stable income.

Security and Fund Utilisation

Both NCD options are secured.

The company has confirmed that there has been no delay or default in payment of interest or repayment of principal related to these securities.

This point matters because payment history often influences investor confidence. A clean repayment record supports the company’s reputation in the debt market.

Shriram Finance has also confirmed that 100% of the funds raised through this issue will follow RBI requirements and all other statutory guidelines.

This statement gives additional comfort regarding the intended use of proceeds. Companies normally disclose such information so investors understand how fresh capital will support business operations.

Why Companies Raise Money Through NCDs

Every financial institution requires regular access to capital. Lending companies borrow funds and then lend those funds to customers.

Shriram Finance operates across several lending segments that require continuous financial support. Fresh borrowing helps the company maintain liquidity and support future business opportunities.

NCDs also allow companies to match the tenure of their borrowings with the tenure of their loan portfolio. This improves financial planning and reduces pressure from short-term funding needs.

Another advantage comes from funding diversification. Companies that borrow through banks, bonds, deposits, and NCDs usually have greater financial flexibility because they are not dependent on one single funding source.

What the Coupon Rate Shows

The coupon rate represents the fixed annual interest paid to investors.

The first option offers 7.80% per annum.

The second option offers 8% per annum.

The difference appears small, yet investors also consider maturity period, issue price, credit quality, and yield before making an investment decision.

A higher coupon does not always mean a higher effective return because the purchase price also influences overall yield.

Understanding the Yield Difference

The first option carries a yield of 7.80%.

The second option carries a yield of 7.90%.

Although the coupon stands at 8%, the effective yield differs because the issue carries a premium issue price of ₹3,370 per debenture.

Yield gives a better picture of the actual return after considering the purchase price. Therefore, many institutional investors focus more on yield than coupon alone.

Maturity Comparison

The first option matures on September 07, 2029.

The second option matures on December 26, 2031.

The first series therefore has a shorter investment period, while the second series extends for a longer duration.

Investors usually choose between shorter and longer maturities based on their cash flow needs, interest rate expectations, and investment strategy.

What This Means for Investors

This issue provides two fixed-income choices with different maturity periods and face values.

Investors who prefer shorter tenure may find the first option more suitable.

Those who seek a longer investment period may prefer the second option.

Since both issues remain secured, investors receive additional comfort regarding repayment support.

Still, every investment decision depends on an individual’s financial goals, tax situation, liquidity needs, and risk appetite. Investors normally review all offer documents before making any commitment.

Possible Impact on Shriram Finance

Successful completion of a ₹2,000 crore fund raise reflects the company’s ability to access the debt market.

Fresh capital strengthens liquidity and provides additional financial resources for lending activities.

A stable funding base often supports long-term business expansion. It also allows better management of future funding requirements.

The market generally views successful debt issues as a sign that investors remain willing to lend money to the company. However, the long-term impact depends on how efficiently management deploys the capital and whether lending operations continue to generate healthy returns.

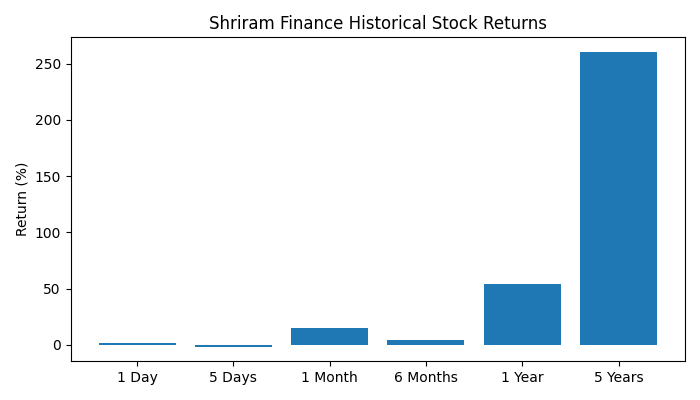

Historical Stock Performance

Shriram Finance has delivered different returns across various time periods.

The stock gained 1.71% in one day.

It declined 1.56% over five days.

It gained 15.06% in one month.

It delivered 3.91% over six months.

The one-year return stands at 54.23%.

The five-year return stands at 260.34%.

These numbers show strong long-term performance despite normal short-term market fluctuations. Stock prices move because of several factors such as earnings, interest rates, economic conditions, market sentiment, and company-specific developments.

Past performance also does not guarantee future returns, so investors usually combine historical performance with business fundamentals before reaching any investment decision.

Overall View

Shriram Finance has successfully completed a ₹2,000 crore fund raise through two secured NCD issues with coupon rates of 7.80% and 8%.

The first issue offers a maturity date of September 07, 2029, while the second matures on December 26, 2031. Both issues provide annual interest payments, remain secured, and carry no record of delay or default in payment of interest or principal.

The company has also confirmed that the entire amount raised will follow RBI requirements and other statutory guidelines. This supports transparency regarding fund utilisation.

From a business perspective, the transaction expands the company’s funding base and strengthens financial flexibility. From an investor perspective, the issue offers fixed annual income through secured debt instruments with different maturity choices.

This article is only an analytical summary based on publicly available information. It should not be treated as investment advice, a recommendation to buy or sell any security, or a prediction of future financial performance. Investors should review official offer documents and consult a qualified financial adviser before making any investment decision.

ALSO READ: Sandur Manganese Adds Two New Independent Directors to Board